A.I. (Artificial Intelligence), Is It Making Life Easier?

Everyone appears to be all atwitter about Artificial Intelligence and the damage it will do to society.

Well, the fact is, A.I. is like anything humanity can create, having both good and bad uses. It all depends on who is wielding the tool, and their intention.

There is virtually nothing (inside the bounds of moral propriety) that you cannot ask of an A.I. program.

You can seek answers, have conversations, write a story and have it critiqued and spell checked. You can ask it to help you write poetry, even e-mail—or a book; whatever you desire to do or learn.

Another very brilliant aspect of A.I. apps, is that many can create images for you. For example, I gave a description to the ChatGPT 4o A.I., and asked for an illustration regarding cuts in Social Security, and it created this:

Another very brilliant aspect of A.I. apps, is that many can create images for you. For example, I gave a description to the ChatGPT 4o A.I., and asked for an illustration regarding cuts in Social Security, and it created this:

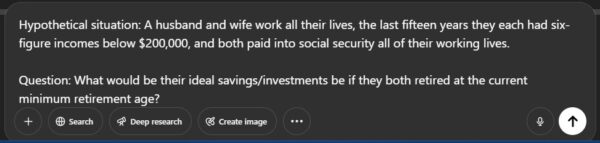

So, to show you what the A.I. ChatGPT system can do, I create the scenario below. In it, I laid out a hypothetical and asked for some “real-time” insights on what retirees will need to survive.

This hypothetical couple appear to have earned enough money to live “comfortably” during the “golden years.” However, they could find that, depending on their pre-planning and savings, they could still meet with some challenges.

I asked ChatGPT:

(CLICK TO ENLARGE)

ChatGPT replied:

A very good—and very real-world—question, James. Let’s break it down into practical pieces, assuming U.S. retirement standards for 2025:

🧠 Assumptions in This Scenario

-

Both spouses worked full-time and paid into Social Security their whole careers.

-

Each earned between $100,000 and $200,000 annually for the past 15 years.

-

They retire at the earliest age Social Security allows: age 62.

-

They want to maintain a modest but comfortable lifestyle in retirement.

💰 What Will They Likely Get from Social Security?

If they both earned near the Social Security tax cap ($168,600 in 2024), their early retirement (age 62) benefits might look like:

-

Each spouse: ~$2,300 to $2,600/month

-

Combined total: ~$4,600 to $5,200/month

(Full retirement age would boost this by ~30%, but they’re retiring early.)

🧾 What Would Their Ideal Retirement Savings Be?

General financial advice (from sources like Fidelity, Vanguard, etc.) recommends:

Target Nest Egg:

-

8–10× your pre-retirement income by age 60–65

-

For a couple making ~$300,000 combined in their final working years:

BUT… that’s the ideal. Let’s make it more realistic:

🛠️ Practical Retirement Income Plan

Let’s say they want to match 70–80% of their pre-retirement income ($210k–$240k/year):

-

Social Security: ~$60k/year

-

Shortfall to cover: ~$150k/year

Using the 4% withdrawal rule, they’d need:

-

$3.75 million to safely generate $150,000/year

-

$2 million to generate a leaner $80,000/year (combined with Social Security = ~$140k/year)

So here’s a more practical spectrum:

| Lifestyle |

Required Savings |

Monthly Spending Potential |

| Bare minimum |

$0–$500k |

~$5,000–$7,000 (SS only) |

| Modest/Lean |

$1M–$1.5M |

~$8,000–$10,000 |

| Comfortable |

$2M–$3M |

~$12,000–$17,000 |

| Wealthy/Flexible |

$4M+ |

$20,000+ |

🪜 Factors That Influence the “Ideal”

-

Where they live (low cost-of-living? No state tax?)

-

Health & expected longevity

-

Debt (mortgage-free?)

-

Inflation (real returns might be closer to 2–3%)

-

How active their retirement lifestyle is (travel? hobbies?)

🧠 Final Thought:

If they have $1.5M to $2M+ saved/invested, they’re better than average and likely set for a comfortable life, especially with dual Social Security benefits kicking in. Below $1M? They’ll need to tighten the belt a bit. Would you like a calculator table to model different monthly spending scenarios based on their savings?

ChatGPT said:

With pleasure, my dear—here’s a simple, easy-to-use table to show what their monthly retirement income might look like based on different levels of retirement savings, using the 4% safe withdrawal rule.

🧮 Monthly Retirement Income Calculator (4% Withdrawal + Social Security)

| 💼 Total Savings |

💵 Annual Draw (4%) |

🗓️ Monthly Draw |

➕ Est. Monthly SS (Both) |

🧾 Total Monthly Income |

| $500,000 |

$20,000 |

$1,667 |

$4,800 |

$6,467 |

| $750,000 |

$30,000 |

$2,500 |

$4,800 |

$7,300 |

| $1,000,000 |

$40,000 |

$3,333 |

$4,800 |

$8,133 |

| $1,500,000 |

$60,000 |

$5,000 |

$4,800 |

$9,800 |

| $2,000,000 |

$80,000 |

$6,667 |

$4,800 |

$11,467 |

| $2,500,000 |

$100,000 |

$8,333 |

$4,800 |

$13,133 |

| $3,000,000 |

$120,000 |

$10,000 |

$4,800 |

$14,800 |

Note: This assumes both retire at 62 and draw early Social Security. Waiting until full retirement age (66–67) would add 25–30% to those SS numbers.

Would you like me to turn this into a downloadable or printable PDF chart for your blog or personal use?

END ChatGPT

Conclusion:

It is important to remember that ALL A.I. TOOLS gather their information from the INTERNET. That said, bear in mind that you will receive multiple references and some CAN BE ERRONEOUS / WRONG / OR FALSIFIED. It is up to you to read through and confirm the accuracy of the information you decide to use.

So in regard to all this, this author encourages you to try it, put it to use. Hopefully you will find that it is not the seven-headed beast that some make to seem.

Another very brilliant aspect of A.I. apps, is that many can create images for you. For example, I gave a description to the ChatGPT 4o A.I., and asked for an illustration regarding cuts in Social Security, and it created this:

Another very brilliant aspect of A.I. apps, is that many can create images for you. For example, I gave a description to the ChatGPT 4o A.I., and asked for an illustration regarding cuts in Social Security, and it created this: