How Much Retirement Income Is Enough For You?

On a scale of 1 to ∞ – how much you “need” to retire is not the same as “how you want” to retire!

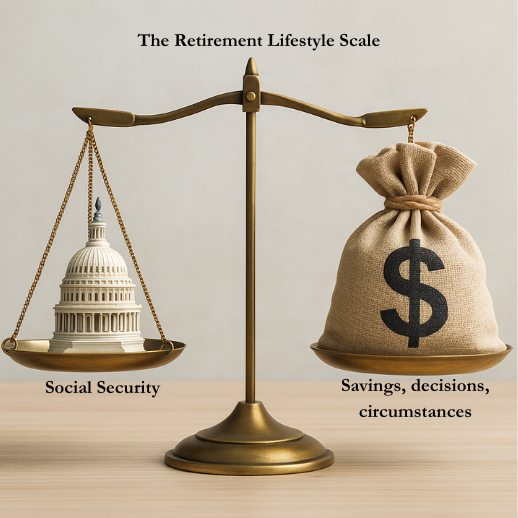

On one side of the retirement lifestyle scale is: “the Social Security program.”

On the other side of the retirement lifestyle scale are: “your personal savings, decisions, and circumstances.”

Key Highlights from Kiplinger

1. Average Monthly Benefit by Age, Without Adjustments

Kiplinger breaks down average Social Security monthly benefits by specific ages for retired-worker beneficiaries, excluding early reductions or delayed retirement credits:

| Age | All Retirees | Men | Women |

|---|---|---|---|

| 66 | $2,127.06 | $2,365.32 | $1,874.97 |

| 67 | $2,162.83 | $2,393.41 | $1,914.87 |

| 70 | $2,176.76 | $2,399.78 | $1,939.61 |

| 75 | $2,174.20 | $2,379.00 | $1,926.64 |

| 80 | $2,250.80 | $2,485.27 | $1,964.84 |

| 85 | $2,202.04 | $2,441.78 | $1,908.60 |

| 90+ | $1,663.04 | $1,730.21 | $1,615.04 |

| Source: Kiplinger – What Is the Average Social Security Check by Age? | |||

Retirees are somewhat like snowflakes; no two of them are exactly alike. In a retirement community of 506 homes, such as ours, you will find anything from retired accountants to zoologists. However, you will not find any two of them with exactly the same retirement income because all of them approached retirement differently.

“How much retirement income is enough for you?”—is the question you need to answer.

Approach Retirement With ‘Speculation,’ Not Expectation!

Pragmatically speaking, when and how you will retire is ultimately determined by several things, including: your earnings over the years, the amount of savings you can accrue, the amount of debt you incurred, your housing, medical, and physical situation, and whether or not you are willing to continue to work after retirement! (My words)

You must consider the fact that “what may suffice for today,” can, and does change rapidly as you continue to age. In other words, it is possible to outlive your income. So that is another very heavy item to take into consideration.

You can locate sound advice from all quarters of the investment world, all of which will include the following—

Sage Advice From a Man Who Knows:

Rob Williams: Managing director financial planning, retirement income, and wealth management, recently published in a 2025 Schwab article:

There are “6 Things to Do If You’re Nearing Retirement.” Below is a brief synopsis of Mr. William’s recommendations:

#1: Find out where you stand

If you don’t have a retirement plan yet, now is a good time to create one, no matter how young or old you are.

If you do have one, check it at least once a year to make sure it still matches your needs and goals. There are a number of items that could change, such as your retirement date, expected future expenses, savings, investments, and potential income sources.

(See the full article for complete information.)#2: Boost your savings, if you need to

Whether you find yourself in catch-up mode or just want to save as much as you can before you stop working, you have options.

—Mr. Williams mentions, an employer-sponsored account—into which both you and your employer can contribute toward your goals.

“…or if you don’t have an employer account—consider… a traditional IRA or Roth IRA. With make catch-up contributions to your IRA starting the year you turn 50.

There is also a possibility of starting a “Health Savings Account (HSA) for future health care costs—with catch-up contributions are allowed starting the year you turn 55.

He goes on to mention: there’s no limit on how much you can save in (your own brokerage)…accounts.

(See the full article for complete information.)#3: Plan ahead for Social Security

While you can start taking Social Security as early as age 62, doing so triggers a reduction in your retirement benefit. If you can wait, your future benefit grows. Once you hit “full retirement age” (between age 66 to 67) your Social Security income will increase up to 8% for every year you delay, until you reach age 70.

(As I mentioned above) Of course, the decision on when to take Social Security depends on your specific situation, including your other income sources, health, and your spouse’s needs and circumstances.

(See the full article for complete information.)#4: Consider tax-smart strategies now

When you’re still saving for retirement, it’s important to prepare for the taxes you’ll end up paying once you reach retirement.

- If you’re in a lower bracket (0%, 10%, or 12%),

- If you’re in a middle tax bracket (22% or 24%)

- If you’re in a higher tax bracket (32%, 35%, or 37%),

It may make sense to maximize your tax-deferred accounts—such as your 401(k), 403(b), 457(b), or Thrift Savings Plan.

Should you consider a Roth conversion before you retire? …

(See the full article for complete information.)#5: Get a head start on future health care costs

Medicare … won’t cover everything, and there are out-of-pocket costs.

About 60% of people will also need some form of long-term care at some point, and the costs can be high.

(See the full article for complete information.)

#6: Start thinking about retirement income

“Happily Ever After” costs about 2.5 Millions dollars.

This author was one that lived WITHOUT INVESTMENTS … Not because he was too cheap! He had a wife and four children to raise.

Still in their fifties, and still investing heavily in their children’s lives, it wasn’t until the later working years that he and his wife were able to start putting anything away for “retirement.”

By that time, the going rate for “Happily Ever After” was about $2.5 Million in the bank.

In his mid-50’s before he reached for a higher education, which in turn boosted his income: suddenly, savings became possible. But too little, too late, and nowhere near the million $$$ range.

Finally approaching a broker with their 401k’s and savings tucked under their arms, they were given a pretty booklet full of charts and bar-graphs. The booklet, in NOT so many words, laughingly suggesting that the couple could, perhaps, take on three more jobs beside the two they had, and retire at age 70.

Regardless: They could not come even close to the $millions$ range.

So the best you can do—is to do the best you can.

Sadly—that $2.5 Million retirement rate—is now DOUBLED, according to some! (See: PNW—Living The American Dream) By: Michael Snyder/Economic Collapse Blog

That, all said, is why this author writes with people like us in mind: i.e., people who haven’t the resources to put away the maximums necessary to attain “The American Dream.”

Most of us had our basic educations, opted for the trades, hospitality services, food services, transportation and logistics, and service and care professional, etc., We were not afforded the opportunity to max our our investment allowances each year, and we had no Daddy Warbucks to ensure that we had a ‘portfolio.’

In other words, we who make up: THE BACKBONE OF WORKING SOCIETY. So the best you can do—is to do the best you can. Save where and when you can, keep you debts low and your heath and well-being high. Once you’ve done everything possible, time will take care of the rest and you WILL manage.

Our best wishes to all…

IF YOU WOULD LIKE TO SUBSCRIBE OR COMMENT:

Share This Story:

Leave A Comment

You must be logged in to post a comment.